Wondering how much your home is really worth, and want some numbers to back it up? A comparative market analysis (CMA) is the secret tool real estate pros use to help determine the ideal asking price of a property.

A well-prepared CMA can significantly improve the chances of a successful transaction. It ensures that the property is priced strategically—not too high to deter potential buyers, nor too low to undercut the seller's potential return.

Here’s everything you need to know about CMAs in real estate, complete with a step-by-step guide on preparing a CMA yourself and a real-world example of a template used by realtors.

Need an agent to help you with a CMA? Clever Real Estate is the best way to find experienced local agents who know the market and can choose the best comps for your home. Take a short quiz to find an agent today!

What is a CMA in real estate?

In real estate, a comparative market analysis (CMA) is a tool used to estimate a property’s fair-market value. It is done by comparing and analyzing a house to similar nearby homes (also called comps, short for “comparable homes” or “comparables”) that have sold recently, typically within the last three to six months.

A CMA helps sellers set a competitive and realistic listing price, which helps attract the right buyers without losing money on the deal. For buyers, it ensures they make informed offers and avoid overpaying for a property.

Free online estimators, such as tools on Zillow, can provide a starting point for sellers and buyers. However, a professional comparative market analysis will prove itself more accurate because it uses the most recent local market data and expert adjustments.

How to run a CMA on your home (DIY guide)

If you’re selling your home FSBO, you can do your own CMA to help you arrive at the perfect listing price. Try to take a step back and evaluate your home objectively by following these steps:

- Gather recent sales data in your area. Use sites like Zillow or Realtor.com to find properties sold in your area in the past 3-6 months.

- Filter for similar properties. Look for homes with similar characteristics to your place: number of bedrooms and bathrooms, age, home type, and square footage (aim for houses within about 500 sq. ft. of your place).

- Identify the most comparable homes. Pick three properties that most closely match your own. Review any available photos to assess interior and exterior conditions and upgrades, which can influence a home’s value.

- Calculate the value. Average the sale prices of your selected comps. For example, if they sold for $400,000, $425,000, and $450,000, calculate the average ($425,000, in this case) to estimate your home’s value. Alternatively, you can calculate the price per square foot for each comp. For instance, if a home sold for $400,000 and is 2,000 square feet, the price per square foot is $200. Multiply this number by your home’s size.

- Adjust for differences. If your home has features not present in the comps, such as an extra bathroom or an outdoor patio, or vice versa, adjust the value up or down accordingly.

This DIY approach provides a useful estimate and starting point. But remember, a professional CMA from a real estate agent can offer far more precision due to access to the latest market data and valuation expertise.

How real estate agents create a CMA

To create a professional CMA, most real estate agents use a similar process. However, they have access to more robust tools, a lot more data, and a depth of local market knowledge. Some main differences include:

- Access to MLS data: Agents can pull recent sales, pending sales, and even listings withdrawn from the Multiple Listing Service (MLS) for more reliable and accurate data than you might be able to find publicly.

- Local expertise: A broker will know which comps are the most relevant and can factor in insights such as neighborhood trends, days on market, and a property’s pricing strategy.

- Detailed adjustments: Thanks to hands-on experience, real estate agents can adjust for differences between properties with more precision. This includes factoring in elements such as upgrades, amenities, lot size, or even intangible aspects, such as curb appeal.

Most real estate agents provide a free CMA as part of a listing presentation to prospective sellers to win their listing. Before each agent visits your property, request that they provide a CMA. By comparing these analyses, you can better understand your home’s market value and discern which agents use a professional approach to deliver an accurate valuation.

What makes a good comp?

A good comp is a property that closely matches yours in multiple criteria — the more similar the comps (and the more similar comps you have), the more accurate your CMA will be.

Of course, finding an exact match among comps is rare. Agents usually identify homes with similar (but not identical features) and make necessary adjustments to the valuation.

Here's how your realtor might determine the closest comps and make adjustments to estimate your home’s fair market value:

- Age of the home: Agents seek properties that are close in age to yours, usually within a few years, to ensure comparable depreciation and upkeep factors.

- Location: Proximity is key. Agents ideally look for comps within a one- to two-mile radius, prioritizing homes in the same neighborhood or subdivision.

- Type of home: The structure type is considered to ensure like-for-like comparisons. For instance, a single-family home is compared with another single-family home, and similar architectural styles are preferred whenever possible to maintain consistency.

- Bedrooms and bathrooms: A critical part of any comp analysis, brokers match your home’s number of bedrooms and bathrooms with similar properties or adjust valuations based on differences.

- Square footage: The size of the living space significantly influences valuation. Agents calculate the price per square foot of recently sold homes in your area to align with your home’s square footage.

- Lot size: Acreage plays a significant role in property valuation. Larger lots typically command higher prices, though adjustments are made based on the home's condition and age.

- Upgrades: Recent renovations, such as remodeled kitchens and baths, can significantly affect a home’s value. Brokers can assess upgrades that online estimators (like Zillow’s) will not be able to reflect accurately.

- Amenities: Features like swimming pools, gyms, and clubhouses, especially those within an HOA community, add value and are considered part of the home’s valuation.

Limitations of a CMA (and how to improve its accuracy)

While a CMA requires a lot of work with numbers, it also includes a fair amount of approximation. A CMA may not be perfectly accurate, especially when done on your own. Here are some main pitfalls to be aware of when calculating a CMA.

Insufficient sales data

A comparative market analysis is only as accurate as the most recent sales data. It’s a real challenge to value a home accurately if no properties in the area have sold recently.

Also, many imprecise CMAs miss recently withdrawn and expired listings. As Amelia Robinette, a principal broker at NoVa House and Home, shares, “Those are important so one can understand what pricing and marketing strategies didn't work.”

Inaccurate or outdated comps

Homes with rare features or in rural areas might lack good comps. In this case, you might be tempted to include less similar properties or those sold more than six months ago. However, this approach can hurt your valuation and reduce its accuracy, as these homes will not represent your situation well.

Ideally, including more comps in your CMA (if they are truly high in quality) is recommended, as this will improve its reliability.

Rapidly changing markets

CMAs only rely on recent sales and don’t take into consideration current market shifts. If the real estate market is stable, a property sold six months ago can be a decent representation of value.

That said, in some cases, the real estate market can quickly become unrecognizable — the COVID-19 pandemic is one of the most obvious recent examples. That’s why it’s crucial to follow the state of the local and national markets if you want your CMA to be as accurate as possible.

Emotional bias in FSBO pricing

Some owners who run a CMA on their property may struggle with emotional bias when pricing their homes. The issue can go either way: some sellers may underprice the property, hoping for a quick sale, which could lower the potential profit. Others may list a home above its true market value due to emotional attachment, making it harder to sell and attract serious buyers.

Lack of experience

A CMA’s accuracy heavily depends on the experience of the person preparing it. An experienced local realtor with knowledge of current market trends will know the best comparables to choose and how to adjust home values properly. In contrast, those who’ve never worked on CMAs before may misinterpret data or overlook crucial adjustments, resulting in inaccurate valuations.

For the most reliable CMA, it’s best to leverage the experience of a seasoned real estate professional. Even if you prepare your own analysis, you can always ask for a second opinion.

Using Clever, you can get a free CMA from a top local agent and price your home accordingly.

CMA vs. appraisal vs. BPO: What's the difference?

| Report | CMA | Appraisal | BPO |

|---|---|---|---|

| Prepared by | Real estate agent or self-prepared | Licensed appraiser | Real estate broker or agent |

| Cost | Free | $400–$600 | $50-150 |

| Detail level | Moderate | Highly detailed | Moderate |

| Used for | Setting a listing or offer price | Mortgage approval, legal matters | Mortgage approval (in certain states), quick valuations |

| Requirement status | Voluntary (although recommended) | May be required by mortgage lender or state laws | Voluntary, unless requested by a lender |

A CMA report is typically used to estimate a home's market value, but it cannot replace an official appraisal. A broker price opinion (BPO) lies in between the two; A BPO is more detailed than a CMA, but also cheaper and easier to obtain than an appraisal.

An appraisal is a detailed evaluation of the home's interior and exterior performed by certified, unbiased professionals. Appraisals are required by mortgage lenders, so they are typically conducted by the buyer after signing a purchase agreement, but before closing. However, a homeowner can always order an appraisal.

A broker price opinion (BPO) is a paid agent-prepared report that can be used by FSBO sellers or in certain situations where a formal appraisal is not necessary (foreclosures or short sales).

Both a CMA and a BPO are based on comparable sales, so appraisals can be particularly beneficial in cases where there are no comparable sales, such as in rural areas or for unique homes, even if not legally required.

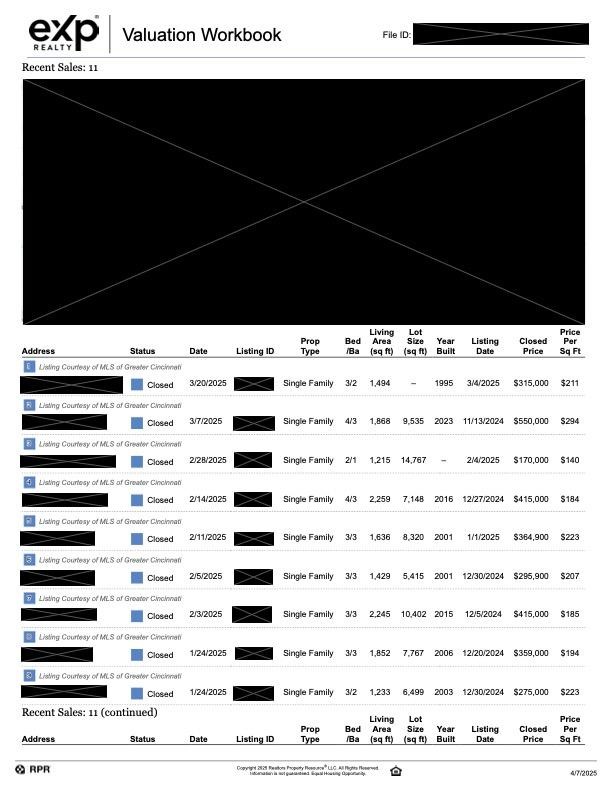

Comparative market analysis example

Christina Scavone, an eXp real estate agent, provided us with a real-world example of a comparative market analysis:

Each row includes information about nearby recent sales, including the sold price, list date, sold date, bedrooms, bathrooms, year built, square footage, and other attributes.

Based on the CMA, Scavone set the subject property’s value at $415,000.

Note: CMA reports may look different in other markets or states, but they all include the same basic information.

FAQ

What is a CMA in real estate?

A CMA in real estate is a report that real estate agents put together to estimate a home’s value based on comparable homes in the area that were recently sold. Many agents present a CMA when they are looking to sign a client to demonstrate their value to the sellers.

What does a CMA include?

A typical CMA lists three to six comparable homes. The report includes a photo of each home, plus a list of key data, such as a property’s original list price, days on market, final sale price (if the property has been sold), number of bedrooms and bathrooms, square footage, year built, and acreage. CMAs may also include any adjustments made to the value of each property.

How is a CMA different from the Zillow Zestimate?

While online home value estimators like Zillow's Zestimate offer a quick glimpse into your property’s potential value, a CMA from a real estate agent generally provides a more accurate reflection of the market based on up-to-date local market data and expert adjustments.