The FHA streamline program is a refinance program that is available to homeowners with an FHA mortgage. The FHA streamline has two streamline options. The non-credit qualifying and credit qualifying mortgage. The term “streamline” refers to the amount of paperwork required to process the new FHA home loan. Let’s take a look at both programs to see which program is best for you.

Both non-credit qualifying and credit qualifying streamlines do not require an appraisal. That’s good news if your home is located in an area with depressed property values. Most refinance programs require some amount of equity as a condition of the refinance. But not the FHA streamline program.

Ownership Requirement

Homeowners are eligible for a streamline refinance loan without credit qualification if all individuals on the present mortgage remain as borrowers on the replacement mortgage. Mortgages that have been assumed are also eligible provided the previous borrower was discharged from liability.

Exception:

The borrower on the existing mortgage may be removed from the title (deed) and the new streamline mortgage in cases of divorce, legal separation or death when:

the divorce decree or legal separation agreement awarded the dwelling and obligation for the monthly payment to the remaining borrower, if applicable; and

the remaining borrower can prove that he/she/they have made the mortgage payments for a minimum of six months prior to the FHA streamline case number assignment.

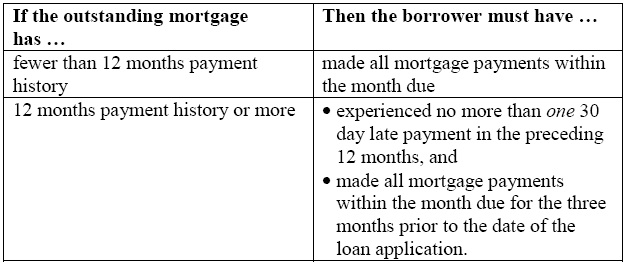

Mortgage Payment History Requirement for a Streamline Refinance

The borrower must have made at least six payments on the FHA mortgage being refinanced and a minimum of six full months is required to have passed since the first monthly payment due date of the mortgage, and at least 210 days must have passed from the closing date of the mortgage being refinanced. A delinquent mortgage is not eligible for streamline refinancing until the loan is brought up-to-date.

Example: The FHA loan case number on the mortgage being refinanced was settled on or before December 1st, and the borrower’s first mortgage payment on that

mortgage was due on January 1st. The lender may request an assignment of an

FHA case number for the refinancing mortgage no earlier than July 1st.

The non-credit qualifying streamline loan does not require a credit check, although, the lender may require a credit report to verify that the applicant meets the ownership and payment history requirement.

Income and employment verification is not required with a non-qualifying streamline.

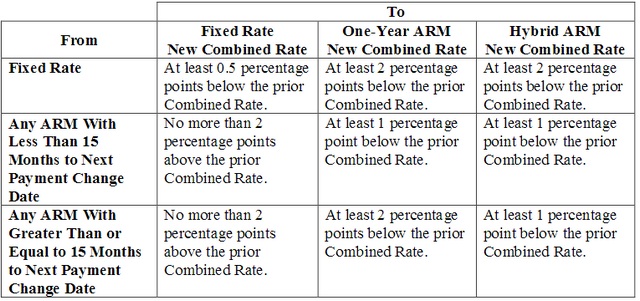

The FHA streamline program requires a reduction in the interest rate

The FHA streamline loan must have a “net tangible benefit”. In other words, the refinance must improve the homeowner’s situation. The net tangible benefit was introduced by HUD/FHA to head off unscrupulous lenders who encouraged homeowners to refinance (usually from one adjustable-rate mortgage to another ARM), that did not benefit the homeowner.

Here are the conditions of the net tangible benefit interest rate test. This chart reflects the interest rate change from the current mortgage to the new mortgage interest rate. The “combined rate” means the new (proposed) interest rate (i.e. 4%, 4.5%, 5%, etc.) plus the monthly mortgage insurance rate (MIP).

Reduction in term

The net tangible benefit test is met if:

- the remaining amortization period (term) of the existing Mortgage is reduced;

- the new interest rate does not exceed the current interest rate;

- and the combined principal, interest, and MIP payment of the new Mortgage do not exceed the combined principal, interest, and MIP of the refinanced Mortgage by more than $50.

Credit qualifying streamline refinance

A credit qualifying streamline occurs when a borrower is removed from the existing mortgage, the remaining borrowercannot prove that he/she/they have made the mortgage payments for a minimum of six months prior to the FHA streamline case number assignment.

Not meeting the net tangible benefit test also requires a credit qualifying refinance. Credit qualifying means the same re-certification of income, monthly debt, credit score and debt to income requirement.

Frequently Asked Questions About FHA Streamline Refinance

Frequently Asked Questions About FHA Streamline Refinance

Q. Are there closing costs for a FHA streamline refinance?

A.Unfortunately, you may have some closing and tax escrow costs with the loan refinance. The Federal Housing Administration prohibits rolling any new closing costs into the new loan, however; some mortgage companies may offer "no cost" refinances by charging a higher rate of interest on the new loan.

Q. Can you cash out on a FHA streamline?

A.No. The FHA streamline program is intended for interest rate reduction.

Q. Do I have to pay closing costs on a FHA streamline refinance?

A.Yes.

Q. Does a FHA streamline refinance require income verification?

A.Since you already qualified for your current FHA home loan, the FHA streamline program does not require additional verification of income or employment for non-credit qualifying streamline refinances; however, some mortgage companies may require one or the other or both verifications.

Q. Do you need an appraisal for FHA streamline?

A.Unlike many loan refinance loans, the FHA streamline program (both non-qualifying and credit qualifying streamlines do not require a home appraisal! This is a great way to refinance your mortgage loan if your home value is less than the mortgage balance.

Q. What documentation do I need for the streamline application?

A.For a non-credit qualifying streamline, the following will be required:

- Most recent bank statement(s) (all pages) to provide proof of funds due at closing. You should also know that large deposits may be required to be documented.

- Copy of your existing mortgage note and the settlement statement (final HUD-1) or Deed of Trust that show the FHA case number of your current loan.

- Copy of your most recent mortgage statement. The statement should contain a break down of your principal and interest payment and monthly mortgage insurance cost. The combination of the P&I and MIP is necessary to estimate the net tangible benefit test.

- Drivers license

- Social security card

Credit qualifying FHA streamline documentation:

In addition to the non-qualifying paperwork, you will also need:

The last two years' W2s (and the last two years' tax returns if self-employed), the most recent paystub(s) documenting the most recent 30 days of income

Q. What is the minimum credit score for a FHA streamline refinance?

A. The FHA non-credit qualifying streamline program does not require a credit check and there is no minimum credit score requirement.