Buying a HUD home can be a smart way to purchase property below market value, but it’s not quite the same as buying a home on the open market. HUD homes come with unique rules, time frames, and financing requirements that buyers need to understand before making an offer.

In this guide, we’ll walk you through what a HUD home is, who can buy one, and each step of the purchase process, including how to find listings, make a bid, and finance your purchase.

💡 Tip: Only a HUD-registered real estate agent can submit a bid on your behalf. Clever Real Estate can connect you with top-rated, HUD-approved agents in your area — and you could get cash back after closing Take a short quiz to get started!

What is a HUD home?

A HUD home is a residential property previously financed with an FHA-insured mortgage that went into foreclosure. After foreclosure, the lender transfers ownership to the U.S. Department of Housing and Urban Development (HUD), which then lists the property for sale on HUDHomestore.gov to recover its losses.

These homes are available to both owner-occupant buyers (those who will live in the property) and, after a set period, investors.

Benefits:

- Often priced below market value

- Eligible for government-backed financing like FHA, VA, or USDA loans

- May qualify for special programs or closing cost assistance

Drawbacks:

The bidding process is competitive and time-sensitive

Sold strictly “as-is” — the buyer is responsible for all repairs

Properties may have been vacant for months and need work

Who should buy a HUD Home?

Buying a HUD home is often a great option for certain types of buyers, such as:

- Low-income home buyers: HUD homes are typically significantly more affordable than open-market listings. What’s more, you could ease home buying requirements by financing the purchase with a low- or no-down payment mortgage (from Fannie Mae, Freddie Mac, FHA, USDA, or VA).

- First-time home buyers: FHA foreclosures might help you buy a home in highly competitive markets that may be unaffordable otherwise. Future owner-occupants have exclusive rights to bid on a home for 30 days, so competition for the property could be considerably lower than the market average.

- Fix-and-flip investors: Distressed properties and markets where HUD has more homes to sell than available buyers can present lucrative opportunities to investors. You must wait at least 30 days before bidding until the “exclusive” listing period is complete.

- Good Neighbor Next Door participants: HUD also offers deep discounts — up to 50% off list price — to teachers, firefighters, police officers, and EMTs who agree to live in the home for at least three years.

6 steps to buying a HUD home

Step 0: Get preapproved for financing

Before you start shopping, get preapproved for a mortgage. HUD requires a mortgage preapproval letter or proof of funds before you can submit a bid.

Preapproval helps your offer stand out and ensures you know your budget. If the home needs major work, consider an FHA 203(k) loan, which combines your purchase and renovation costs into a single mortgage.

Step 1: Find a HUD-approved agent

While anyone can browse the HUD’s available homes, only HUD-registered real estate agents can submit a bid on your behalf. So if you’re seriously considering buying a HUD home, partnering with a dedicated broker is a step you cannot disregard.

There are two ways to find a HUD-approved realtor — first, you can ask the broker you work with if they are registered with HUD (many of them are). If you don’t have an agent in mind, you can search for them using the dedicated tool on the HUD Homestore website. Type in your city or ZIP code, and you’ll see a list of registered brokers in your area with their contact details.

Here are some tips for choosing a HUD-registered realtor:

- Make sure the broker has direct experience handling HUD transactions

- Search for an agent with knowledge of the local market

- Check online reviews or ask a few agents who seem like a good match for references

The right agent will guide you through the distinct requirements on HUD houses, help you make a competitive offer, and walk you through the closing process. Find the realtor you need through Clever Real Estate — 100% free! — and get cash back to help you pay for your move.

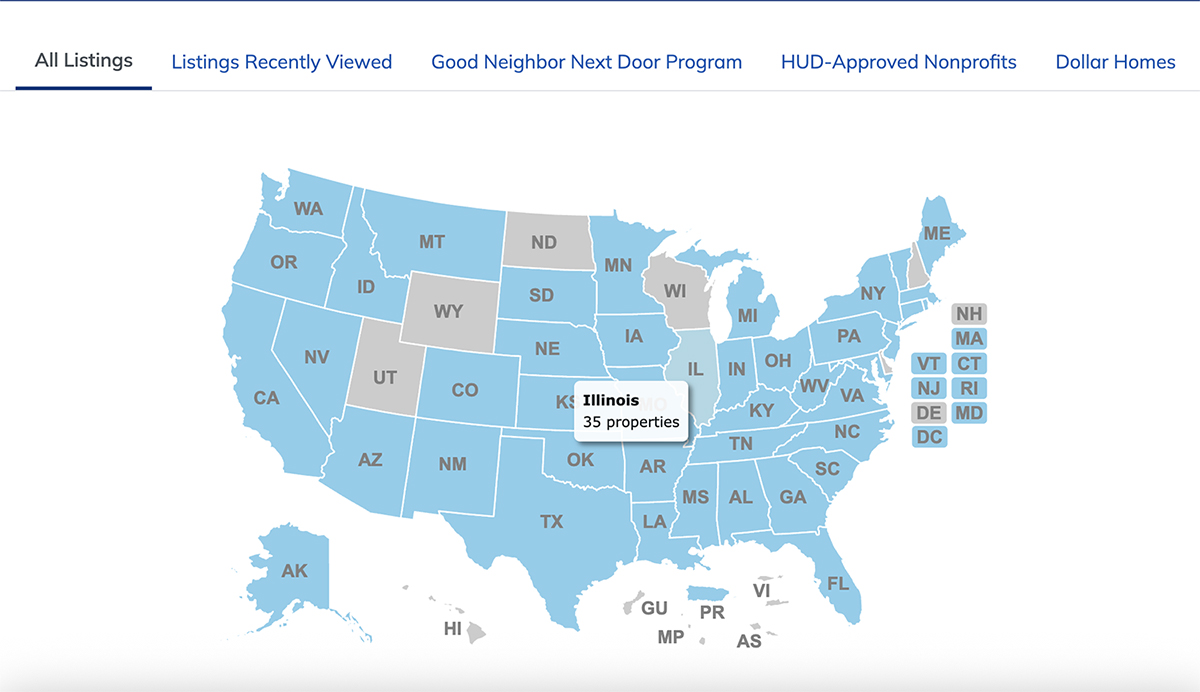

Step 2: Find HUD homes on the HUD HomeStore

To browse for available properties on the HUD HomeStore website, you can use the box on the homepage under “Find a HUD Home” or click on the map on the home page to begin. You can search broadly by state, or narrow down your search by entering a city, ZIP code, or case number.

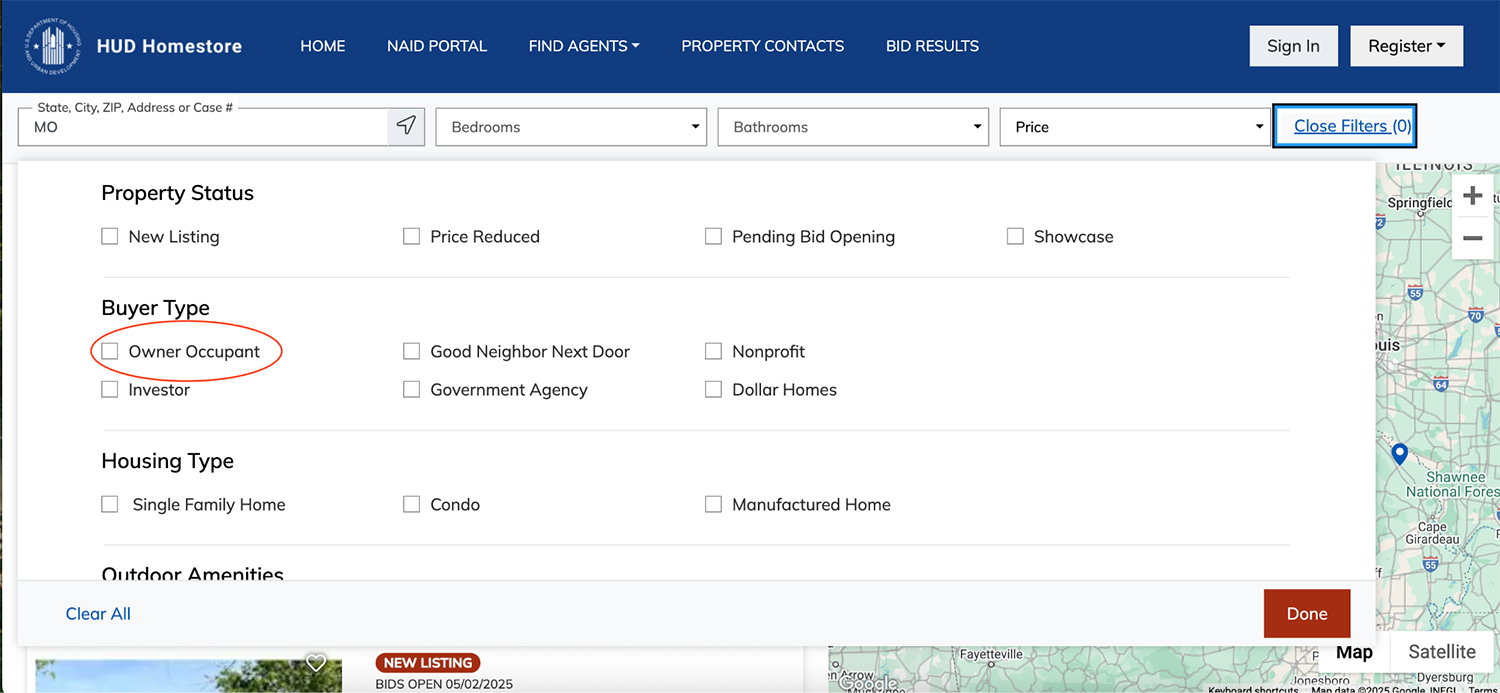

On the following page, you’ll see listings that match your initial selection and an advanced filtering option to further narrow your search. These filters include number of bedrooms and bathrooms, price, property status, buyer type, housing type, amenities, and more.

If you’re a prospective owner-occupant — a buyer who will certify to them that you’ll use the property as your primary residence for at least a year — you have priority bidding for HUD homes during the initial listing period. On the results page, expand “More Filters” and be sure to click “Owner Occupant” under “Buyer Type” to benefit from up to a 30-day priority window.

Here are some tips and tricks for finding a HUD home:

- Check out HUD HomeStore listings daily, as inventory changes frequently and quickly. If you don’t see a home available in your target market, don’t give up, as HUD homes come and go fast. Ask your agent to stay on top of new listings and inform you as they hit the market.

- Broaden your search area to increase your chances. Rather than entering a specific city or postal code to search, search by state, and you may uncover homes you’d have missed because they're located just outside your search zone. Search nearby states, as well, if you’re open to relocating.

- Know if you’re eligible to bid when an ideal home becomes available. The “Listing Period” refers to the length of time a HUD property is open for bidding, and the time period can vary depending on a number of factors. Owner-occupants typically have a 30-day exclusivity period for insured properties, while uninsured properties may only offer a 5-day period.

Listing periods are prominently posted on each entry, indicating who is eligible to bid on a property at a given time. There are several listing periods to understand:

- Exclusive listings are listings in an early bidding period and are limited to owner-occupants, HUD-approved nonprofits, and government agencies.

- Lottery listings are for homes in specific revitalization areas that are eligible for HUD-approved nonprofits, government agencies, and Good Neighbor Next Door participants.

- Extended listings come after the previous periods. During this timeframe, everyone is eligible to bid.

- Dollar homes government sales are listings for vacant homes, which HUD sells to local governments for a nominal fee of $1. These homes have often been on the extended listing period for over six months.

Step 3: Submit an offer

Once you find a home you like and are eligible to buy, it’s time to work with your real estate agent, who can place a bid on your behalf.

How much should you bid on a HUD home? For a house that you’re seriously interested in, bid around 85–88% to start. For example, if you’re bidding on a home listed at $300,000, that’d be a $255,000–264,000 bid.

Make sure to talk to your agent and get their opinion about how much to bid. They will have a better idea of what HUD homes typically sell for in your area.

If HUD rejects all bids for a particular property for not meeting their minimum bid requirements, they may send a counteroffer notice to bidders who took part.

The bidding window for HUD properties tends to have two phases: an initial exclusive period for eligible parties (usually owner-occupants and government agencies), followed by an extended period for all interested bidders. There is a 10-day minimum period for each listing, allowing each property to gain sufficient visibility for interested parties. If there is no winning bid during the exclusive period, bids are reviewed daily in the extended period.[1]

If you win your bid, you’ll be able to request up to 3% of that amount towards financing and closing costs (see Form 9548, Sales Contract, Line 5). HUD may credit this amount to the buyer at closing.

Before submitting an offer, be sure to understand the earnest money requirements. Earnest money is essentially an upfront deposit that’s held in escrow until closing. Earnest money is applied to the purchase price at closing, but it can be forfeited if you retract your offer or otherwise fail to meet any contractual obligations.

Step 4: Understand what "as-is" means

When you’re buying a home via a more traditional route and the home inspection uncovers some larger issues, there is a high chance that the seller will be responsible for the repairs. Even if the problems are minor, you may be able to negotiate with the current homeowner and lower the price or ask them to address the issue at their expense.

However, HUD homes are sold as-is, meaning that regardless of the extent of any problems, the buyer (not HUD) is responsible for repairs. While some HUD properties may be in good shape, others may have been empty or neglected for a long time, which can affect their condition.

To protect yourself against any unpleasant surprises or large unexpected repairs, it’s crucial to get a HUD home professionally inspected. If HUD accepts your bid, you have 15 days to conduct an official home inspection and cancel the contract if you find serious issues with the house.

Step 5: Understand owner-occupant requirements and restrictions

Buying a residential property through the HUD HomeStore program does have some requirements and restrictions, especially when it comes to being an owner-occupant.

To qualify as an owner-occupant, buyers of a HUD property must live in the home as their primary residence for at least 12 months following the purchase.

Both the buyer(s) and their broker must sign a letter certifying their intention to follow through with the owner-occupancy requirements. There may also be a requirement for the buyer to move into their new home within 60 days from closing.

What’s more, to qualify as an owner-occupant bidder, you cannot have purchased a property from HUD in the past 24 months.

Buying as an owner-occupant also comes with some perks. For example, during the exclusive listing period, owner-occupants (as well as government agencies and approved nonprofits) have a 30-day window where they can bid before it opens up to the general public.

Step 6: Financing a HUD home

You need a mortgage pre-approval letter to start bidding on HUD homes. This reduces the risk of a deal falling through for HUD and helps streamline the transaction for both parties.

A HUD home can be financed with a few different types of loans:

- FHA loan: A government-backed mortgage, it has lower credit score and down payment requirements (as low as 3.5%) compared to conventional loans. To qualify, you must use the intended property as your primary residence and meet FHA eligibility criteria.

- VA loan: This mortgage is available to veterans, active-duty service members, and qualifying spouses. Backed by the Department of Veterans Affairs, the VA loan does not require a down payment or private mortgage insurance (PMI), and it offers competitive interest rates.

- USDA loan: This loan is designed for buyers in eligible rural and suburban areas, requires no down payment, and has lower interest rates compared to many conventional loans.

- Conventional loan: This type of loan is available through private lenders. Typically, conventional mortgages require higher credit scores and down payments than government-backed ones.

- FHA 203(k) loan: If a HUD property needs significant work, this program allows buyers to finance both the purchase of the home and the cost of its renovations in a single mortgage.

- Hard money loan: This short-term loan is provided by private lenders and could be a good choice for investors or buyers who may not qualify for traditional financing. However, hard money loans come with higher interest rates, larger down payments, and are generally more suitable for those planning to renovate and resell the property quickly.

Note that each of these loans has distinct eligibility criteria, so it’s important to choose one that will best fit your personal situation and the condition of the property. For example, FHA or VA loans may require homes to meet certain property standards that might not be achievable for all HUD houses.

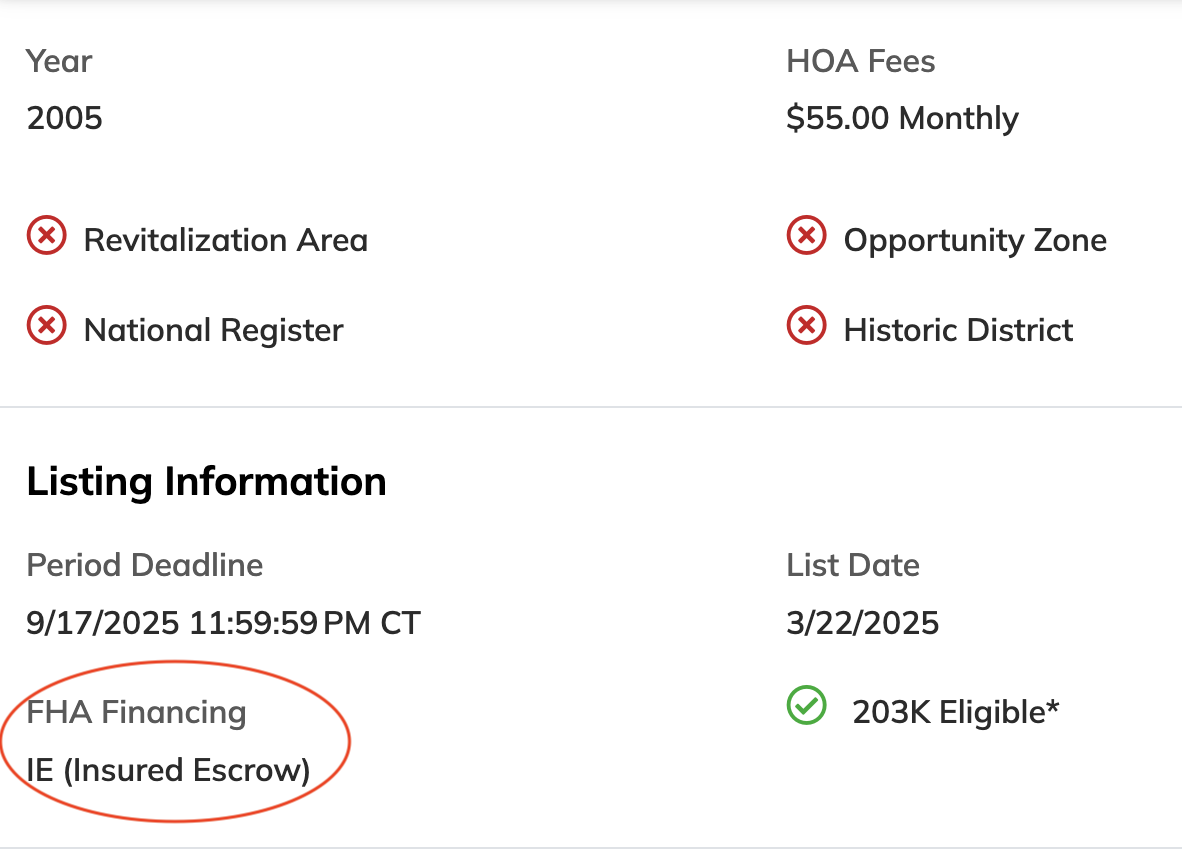

Every home listed on the HUD website for sale has a financing code, which shows whether a property would be qualified for FHA financing:

- Insured (IN) — The home is eligible for an FHA loan. The property needs no obvious or significant repairs, and you can likely buy it with any type of mortgage.

- Insured Escrow (IE) — The home needs basic repairs to meet minimum property standards. The property is still eligible for an FHA loan, but you will need to pay the repair costs up front (deposited into an escrow account at closing).

- Uninsured (UI) — The property needs significant repairs to be livable. These HUD homes are not eligible for FHA financing, but they may still be eligible for an FHA 203(k) loan.

Earnest money deposit

HUD will ask you to make an earnest deposit toward your closing costs with your contract. If the home sale price is:

- $50,000 or less, you’ll submit $500

- Greater than $50,000, you’ll deposit $1,000

Owner-occupants will get their earnest money back if they cancel within 15 days of their contract being accepted. Investors, however, will not get their earnest deposit back.

Closing costs

HUD may pay for some of the closing costs, such as prorated property taxes, HOA fees and transfer fees, recording fees, and overnight mailing charges. What’s more, you can receive closing cost assistance, where HUD may pay up to 3% of the home’s purchase price for:

- Appraisal fees

- Credit report (up to $20)

- Flood certification

- Home inspection

- Home warranty (up to $250)

- Loan origination fees

- Real estate commissions

- Recording fees

- Title insurance

Note that if you want HUD to assist with covering these closing costs, you must request it on Line 5 of Form 9548 (Sales Contract) when you submit your bid. Otherwise, you'll have to cover closing costs yourself.

Pros and cons of buying a HUD home

Pros

- Potentially below-market prices

- Priority bidding for owner-occupants

- May qualify for 3% closing-cost assistance

- Multiple financing options, including FHA and VA loans

Cons

- Sold strictly as-is; repairs are your responsibility

- Competitive and time-sensitive bidding process

- Limited inspection window (15 days)

- Some homes won't meet FHA standards without repairs

Buying a HUD home: The bottom line

Buying a HUD home can be an affordable path to homeownership or an investment opportunity — but it comes with extra paperwork, strict deadlines, and potential repairs. With the right financing and an experienced agent, you can land a property well below market value.

Start by getting preapproved and connecting with a HUD-registered real estate agent who understands the process. Clever Real Estate can match you with top local agents who specialize in HUD transactions — and you could get cash back after closing.