❗ Important Notice

Ribbon Home has paused operations

As of November 2022, Ribbon Home has shut down operations. However, you have other options to help you unlock your equity to buy a new home:

- Consider another buy-before you-sell program: Buy-before-you-sell programs like Knock's Bridge Loan and Orchard's Move First let you borrow against your current home value to buy a new house before you list – without having to cover two mortgages out of pocket. You'll pay program fees alongside typical realtor commissions. You'll also need to be approved for a short-term loan, so if credit is an issue, a buy-before-you-sell program may not be an option.

- Sell to an iBuyer: iBuyers like Opendoor can make you an offer quickly — sometimes in less than 24 hours — and complete the sale in as little as 10 days. However, you’ll typically make a little less than market value on your home while paying 5% or more in service fees.

- Talk to a reputable realtor: If you need to sell fast but don't want to give away your equity to do it, consider working with a top local real estate agent — preferably from a brokerage offering lower commission rates. Even if your house isn’t in the greatest condition, listing on the MLS gives you the greatest chance of getting multiple competing offers. And although a realtor can’t predict exactly when your home will sell, good agents know how to price and market homes to sell quickly.

Just be sure to get a few different opinions before signing anything — accepting the first offer that sounds reasonable can cost you thousands on your home sale.

To save time comparison shopping, you can start with a free service like Clever Offers, which helps you find the most competitive cash offers on your house through a network that includes local investors, iBuyers, and buy-before-you-sell services. They can also give you a professional opinion of your home's current market value to weigh against offers.

Compare cash offers with no obligation and sell in as little as 7 days for the highest cash value.

Ribbon reviews | Costs | Benefits | Drawbacks | Is Ribbon legit? | How it works | FAQs

Ribbon helps you buy a new home before you sell your current one by fronting you the money to make a competitive all-cash offer. Cash offers are more appealing to sellers than traditional financing because they're less likely to fall through. Ribbon charges 1% of the purchase price of the new home for this service.

Ribbon's service fee is lower than the typical buy-before-you-sell service, such as Orchard's 4% fee or Knock's fee of 1.25% plus $1,450. But Ribbon doesn't provide the type of end-to-end service that other companies do to help sell your old home. You'll need to find an agent, secure financing, and do all of the work to sell your old home (including staging and repairs).

| » 🎯 Quick Tip: If you're going to use Ribbon, you'll need an experienced agent on your side to help sell the old home and negotiate the price of the new home. Fortunately, Clever Real Estate can match you with a 1.5% commission agent so you can buy your next home with Ribbon and save thousands on commission. |

Ribbon vs. the competition

Ribbon isn't a full-service buy-before-you-sell program like competitors Knock, Orchard, or Homeward, which help you sell your old home. For example, Orchard and Knock will provide interest-free loans to help you fix up your old home before putting it on the market. They'll also offer to buy your home if it doesn't sell within four to six months and help you find a mortgage for your new home, too.

Ribbon's service doesn't have any of these perks. In fact, Ribbon isn't a lender, nor does it help you find a mortgage. You'll need to come to Ribbon with a pre-approval letter from a lender already in hand.

Ribbon's terms will be easy to follow for most people who are approved for the program, so there's little risk to use the service. It gives you 180 days after you move into your new home to sell your old home and finalize your new mortgage. In most markets, this should be plenty of time.

» GUIDE: Not sure which buy before you sell service is right for you? Check out our guide!

Ribbon services

Ribbon provides three cash offer services with different costs: Ribbon Boost, Ribbon Reserve, and Ribbon Rescue. Your particular situation will determine which is right for you.

Ribbon Boost (formerly Offer Upgrade)

Cost: 1% of home purchase price

This is Ribbon's standard cash offer service. You'll need to be pre-approved by a third-party lender before making an offer. As long as your mortgage is finalized by closing, you'll take ownership of the home right away.

Ribbon Reserve

Cost: 2–2.75% of home purchase price

If your mortgage isn't ready in time for closing, Ribbon Reserve will step in and purchase the house to save the deal. You'll rent the home from Ribbon for up to 180 days until your mortgage is ready.

Ribbon Rescue

Cost: 3.25% of home purchase price

If you've entered into a contract on your own but are having trouble closing because your mortgage is delayed, Ribbon Rescue will save the deal with its cash. You'll then rent the home from Ribbon for up to 180 days until your mortgage is finalized.

Benefits of Ribbon

It's inexpensive

Ribbon's base 1% fee is less expensive than Orchard or Knock's service fees of 4–6%.

You can choose your own agent

This gives you the chance to find an agent that you trust, and even save more with a discount agent.

You can choose your own lender

This could be to your advantage if you already have a lender picked out and have a great rate lined up. Most other companies help you find a mortgage lender — that's how they make their money.

Ribbon will cover an appraisal gap

Before you make a cash offer using Ribbon Boost, Ribbon determines the "Ribbon Max Value" — the most they'll pay for the home. After a seller accepts your offer, a professional appraiser will determine the value of the home. If the appraisal says the house is worth less than the offer, Ribbon will give you the money to cover the gap up to the Ribbon Max Value.

Ribbon can step in with cash to save a deal that's in danger of falling through

Even if you're not working with Ribbon yet and you're already under contract, Ribbon can help. Its Ribbon Rescue service can help you close if you're still waiting on the home loan to be finalized and the seller is getting impatient. The cost for this service is up to 3.25% of the purchase price of the home.

Drawbacks of Ribbon

Ribbon starts out inexpensive, but it can get costly

If your financing doesn't come through in time for closing, Ribbon Reserve will buy the home for you, and your cost will rise from 1% to 2–2.75%. If you're concerned that your old home won't sell before you're ready to close on the new home, and you can't float two mortgages at once, you'll likely have to use Ribbon Reserve.

You'll have to pay rent on the new home

Like other buy-before-you-sell services, you'll lease the home from Ribbon if you're still waiting for financing to be finalized after you move in. Ribbon says the rent will be roughly equivalent to the mortgage payment, plus taxes, insurance, and HOA fees. So you'll be paying to live in the home, but you won't be building any equity.

There's no guarantee that your old home will sell

Lining up the sale of both homes is a problem that companies like Knock and Orchard are better at solving. Also, other buy-before-you-sell services will buy the home from you if it doesn't sell on the open market after a set period of time.

You may lose the new home if there is a problem with your mortgage

If you can't repurchase the home for any reason within 180 days, the lease ends and you have to move out. You will forfeit rent and deposits paid, and Ribbon will sell the home. This could end up being a problem if your old home doesn't sell, as that could prevent you from getting a new mortgage for the new home.

A lot hinges on closing on the new home in time

Some past reviews indicate Ribbon has occasionally been bad at communicating with customers or getting paperwork completed in time for closing.

Who should use Ribbon?

If you're comfortable doing a lot of the work yourself — finding an agent, securing financing, lining up the sale of the two homes — Ribbon could be an inexpensive way to make a cash offer.

Ribbon could be a good solution if you need to close quickly: it claims to be able to close within 14 business days — that's about three calendar weeks.

If you live in states such as Alabama, Missouri, and Oklahoma (where only a few competitors are doing business), Ribbon could be one of your only options.

Ribbon is also good for you if you prefer to find your own real estate agent. Luckily, our partners at Clever Real Estate can help you save by matching you with 1% commission agents, providing thousands in savings.

| 💰 Compare hand-picked agents, get incredible savings!

Find top-rated agents from local brokerages, and get pre-negotiated fees of just 1.5%. Clever Real Estate's service is 100% free, with zero obligation. Find an agent today. |

Is Ribbon legit?

Yes, Ribbon is a legitimate company offering cash offer services to home buyers. Ribbon is NOT a lender, but an underwriter that helps customers find loans they need to buy homes.

The company raised $330 million from investors in 2019[1] and another $150 million in September 2021.[2] It recently launched in Oklahoma, a state where not many other buy-before-you-sell companies operate.

Where does Ribbon operate?

Ribbon currently operates in 11 states: Alabama, Florida, Georgia, Indiana, Missouri, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, and Virginia. In March 2022, the company announced that it would expand into six additional states later in the year.[3]

Ribbon reviews from customers

Ribbon has an A+ rating with the Better Business Bureau, but only a handful of reviews there. On Trustpilot, Ribbon has an average rating of 4.5 out of 5 across 152 reviews. Most of the reviews on Trustpilot (79%) are five-star reviews.

| Trustpilot | 4.5 out of 5 across 152 |

Many Trustpilot reviews are from agents whose clients are working with Ribbon. Overall, customers and agents seem to like the convenience of Ribbon's services.

Positive reviews compliment Ribbon for doing what it says it does: helping customers make competitive offers and win the home. But overall, the positive reviews seem somewhat scripted, frequently mentioning that "reps were always available."

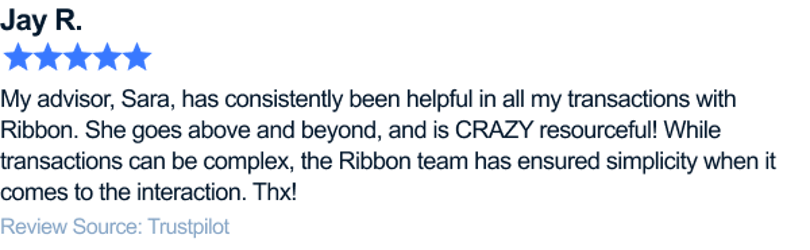

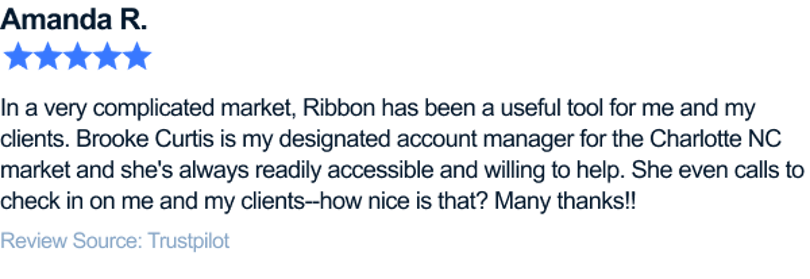

Agents say the company is resourceful and responsive

Five-star reviews written by real estate agents are typically full of praise — but light on specific details.

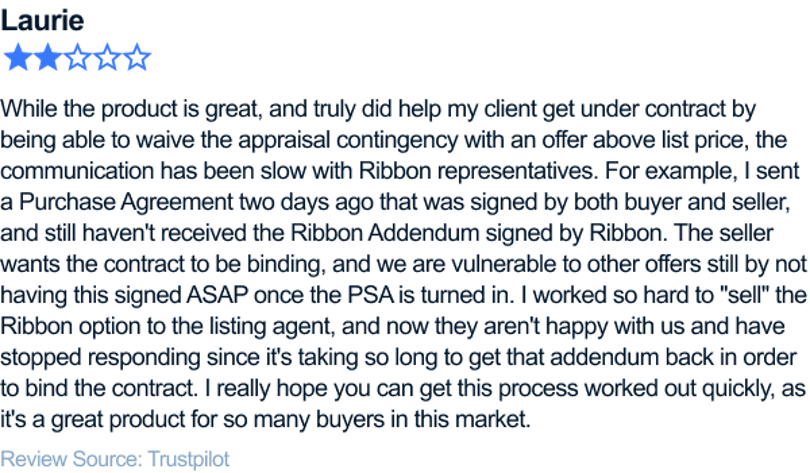

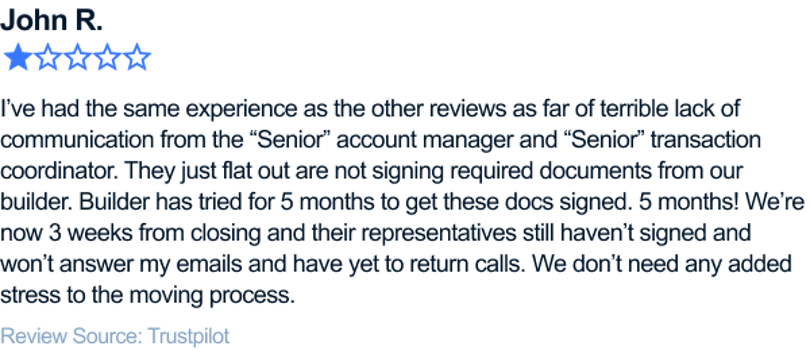

Customers complain about delays and lack of communication

Negative Ribbon reviews on Trustpilot go into more detail.

A cluster of bad reviews from 2021 complain about lack of communication or being unable to get someone on the phone.

In replies, Ribbon apologizes for the delays with variations of "We’re making some significant changes to our workflows to prevent issues like this in the future."

A common theme among these complaints was that Ribbon delayed the process by not completing paperwork. That's more than an inconvenience, since the cost of the service goes up if you can't close on time — you'd need to use the Ribbon Reserve service to purchase the home for you.

For example, this real estate agent liked how Ribbon's service helped their client win the home — but worried about losing the deal because of delays.

One customer worried that the delays would sink the deal on their new construction home.

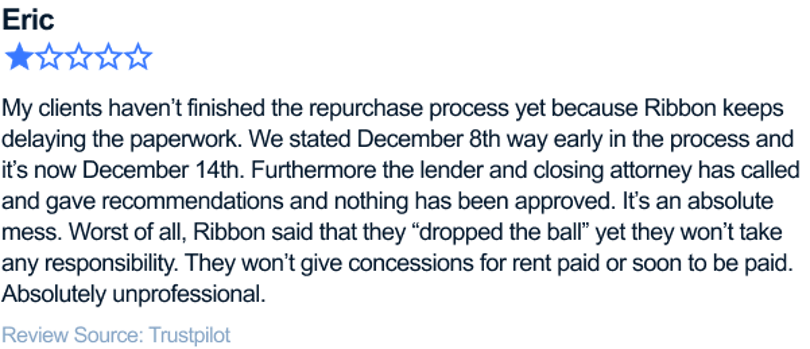

Another agent said the process of repurchasing the home from Ribbon has been "a mess" because of delayed paperwork.

How does Ribbon work?

Ribbon offers two services designed to help you buy a home before you sell yours: Ribbon Boost and Ribbon Reserve.

Ribbon Boost is the standard cash offer service that costs 1% of the home's purchase price. As long as your financing is approved and finalized in time for closing, this should be all you need to buy a house.

If your financing isn't finalized in time, the Ribbon Reserve program kicks in. In this case, Ribbon buys the home and sells it back to you for the same price. You'll pay the Ribbon Reserve costs of 2–2.75% instead of 1%.

Here's how Ribbon works:

- Find a lender and get a pre-approval letter. Ribbon uses the pre-approval letter from your mortgage lender to determine how much it'll lend you for a cash offer.

- Start shopping for homes. Send the homes you're interested in to Ribbon, and the company will tell you the maximum amount it's willing to spend on it — that's the "Ribbon Max Value."

- Make a cash offer using Ribbon Boost. If the seller accepts, and your financing comes through in time for closing, you'll take ownership of the home and start making mortgage payments. Your cost is 1% of the purchase price.

- Use Ribbon Reserve to hold the home (if necessary). If your financing is not ready in time, you use Ribbon Reserve to buy the house. Your cost rises to 2–2.75% of the purchase price. You rent the home from Ribbon until your financing comes through, which may depend on selling your old home. Ribbon allows you to rent the new home for up to 180 days.

Ribbon Boost also provides appraisal protection, which guarantees the contract price up to the "Ribbon Max Value," a predetermined limit that Ribbon will pay for the home. If the home appraises for less than the contract price, Ribbon will make up the difference for no additional fee.

| Ribbon home purchase criteria |

|---|

| Single-family homes, townhomes, condos, or new construction |

| $150,000–1,000,000 |

| ≤4 acres (many other services limit lot size to 1–2 acres) |

| Built after 1960 or fully renovated |

Short sales, foreclosures, or manufactured or modular homes are not eligible. Ribbon will not back purchases for investment properties, only primary residences.

| 👋 Next Steps: Talk to an expert!

If you're weighing your options for buying or selling a house, our partners at Clever can help! Clever's fully-licensed concierge team is standing by to answer questions and provide free, objective advice on getting the best outcome with your sale or purchase. Ready to get started? Give Clever a call at 1-833-2-CLEVER or click to learn more. Remember, this service is 100% free and there's never any obligation. |

How much does Ribbon cost?

Ribbon Boost costs 1% of the purchase price to back your offer with cash

You'll still need to pay an agent commission of 4–6% and buyer closing costs of 2–5% like you would with any home purchase.

If you are confident that you'll be able to find financing and sell your old home quickly, the 1% fee for a cash offer might be worth it in a competitive market.

Ribbon Reserve costs 2–2.75% plus the cost of rent

If your financing doesn't come through in time for closing, Ribbon will purchase the home using Ribbon Reserve. You'll also pay other typical costs like agent commission of 4–6% and buyer closing costs of 2–5%.

You'll also pay prorated monthly rent until you buy the home, which will be roughly equal to the cost of the mortgage payment. The chances of Ribbon needing to step in to purchase the home are higher if:

- You think you'll have trouble getting financing

- Your old home will take longer than average to sell

Ribbon Rescue costs up to 3.25%

If you're already under contract and having trouble finalizing financing, Ribbon Rescue will step in and close with cash for 3.25% of the purchase price. You'll also pay other typical costs like agent commission of 4–6% and buyer closing costs of 2–5%.

You'll also pay prorated monthly rent until you buy the home, which will be roughly equal to the cost of the mortgage payment.

View the complete list of Ribbon Reserve and Ribbon Rescue fees, which vary from state to state.

Frequently asked questions about Ribbon Home

Ribbon is not a lender, but it does help homebuyers make a cash offer on a new home. Homebuyers then take out a traditional mortgage to pay for the home. Read more about how Ribbon works.

Ribbon was founded by CEO Shaival Shah in 2017. Learn more about Ribbon.

Ribbon launched in Charlotte, NC, in 2018. It has since expanded to 11 states and plans to expand further. See where Ribbon operates.

Ribbon determines the maximum value they will pay for a home, called the Ribbon Max Value. After the seller accepts the Ribbon cash offer, a professional appraiser will determine the amount of the home. If the appraisal determines the house is worth less than the offer, Ribbon will step in and give you the money to cover the gap up to the Ribbon Max Value. Learn more about how Ribbon works.